Global Growth Strategy Commentary Q1 2026

Rate Reversal Rewrites Growth Playbook

Key Takeaways

- Geopolitical shocks stalled a solid start to the year for global equities, with value stocks holding up much better than growth as commodity prices soared and inflation risks rose.

- The Strategy underperformed its core benchmark due to a lack of energy exposure and a March selloff in higher-beta technology and financials holdings.

- We actively repositioned the portfolio’s growth exposures, driven by a focus on enhancing participation in secular growth trends, managing risk and leveraging opportunities created by volatility related to the Middle East conflict.

Market and Performance Overview

Global equities declined meaningfully in March as the U.S. and Israel’s military conflict with Iran escalated materially through the month, leading to mixed results for the first quarter after a positive start to the year. The benchmark MSCI All Country World Index finished down 3.2%, with Asian markets sustaining gains while the U.S. and Europe endured losses.

On a regional basis, Asia Ex Japan advanced 3.0%, the United Kingdom rose 2.1% and Japan 1.4% to outperform the benchmark. Emerging markets (-0.2%) also outperformed while Europe Ex U.K. (-4.1%) and the U.S. (4.6 %) declined.

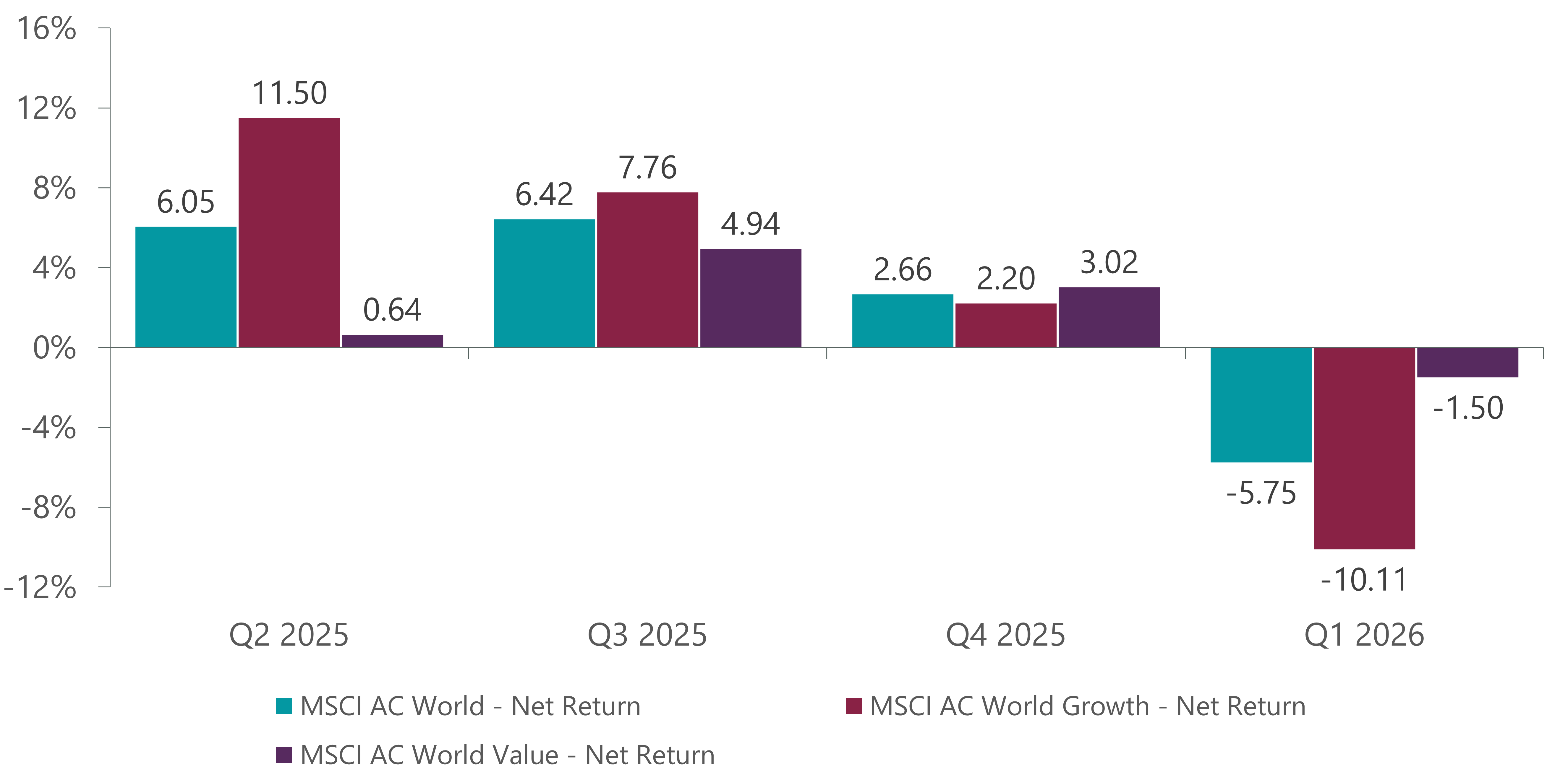

Global growth stocks lagged global value stocks as a U.S.-led rotation out of technology into more cyclically oriented market segments gained momentum in the first two months of the quarter before the conflict dragged everything lower in March. For the three-month period, the MSCI ACWI Growth Index fell 10.1%, and the MSCI ACWI Value Index fell 1.5% (Exhibit 1).

While global markets had been preparing for a period of lower rates, which would have been beneficial to growth stocks generally, rates began to move higher following the start of the Middle East conflict. Equity markets are still grappling with long-term implications of these moves and, most importantly, their duration.

In the U.S., which represents the largest weight in both the benchmark and the Strategy, the first quarter was defined by a sharp shift in market leadership and a material deterioration in investor sentiment with the S&P 500 Index finishing down 4.3%. One of the quarter’s defining features was the emergence of new market leadership. Long-lagging sectors outperformed, reversing the AI-driven momentum that dominated the prior three years. Energy, utilities, materials, industrials, energy, utilities, consumer staples and real estate all outperformed while communication services and information technology (IT) lagged. The labor market appears increasingly choppy while inflation headwinds have become tangible, creating a difficult backdrop for the Federal Reserve.

Exhibit 1: MSCI Growth vs. Value Performance

As of March 31, 2026. Source: FactSet. Currency: AUD.

The Iran conflict created immediate oil and gas supply disruptions that directly affect an energy-dependent Europe already struggling with the cutoff of Russian energy due to the war in Ukraine. Closure of the Strait of Hormuz also raised the risk of higher inflation from commodity price spikes and caused the European Central Bank to reverse course on what was expected to be a continued program of rate cuts.

Portfolio Performance

The ClearBridge Global Growth Strategy underperformed for the quarter. The biggest obstacle affecting relative performance was a lack of traditional energy exposure in a three-month period that saw the energy sector soar 33.6%. Given the selloff in March, higher-beta names in areas such as information technology (IT), financials, consumer discretionary and communication services were most impacted.

Within IT, growing investor disillusionment about the ultimate payoff from massive capital spending on AI buildouts weighed on U.S. mega cap stocks such as Microsoft. The launch of Claude Cowork and other generative AI tools in the quarter also heightened concerns that AI-native solutions could alter competitive dynamics in software and IT services, leading to broad-based multiple contraction in holdings, including location software provider Life360. This dynamic impacted nearly all software companies, including those we believe are relatively well-positioned to benefit from AI, such as advertising tech provider AppLovin, or are less susceptible to disruption.

China’s Tencent was lower as the company has been engaged in a public LLM subsidy battle for market share that also involves Bytedance, the leader in daily active users, and Alibaba, which boasts the largest monthly active user base. Despite this competitive threat, Tencent’s core business areas, including its gaming business, continue to deliver strong growth.

Within financials, HDFC Bank, India’s largest bank, declined as sentiment among Indian companies took another turn lower in the quarter. On top of a rotation out of the region toward areas more indexed to AI innovation, the Iran conflict highlighted India’s dependence on foreign energy to power the world’s fifth-largest economy. U.S. alternative asset manager KKR was down sharply on liquidity concerns in the private credit market, and we sold the position during the quarter.

The Strategy’s industrials exposure offset broader weakness in global markets. Companies supporting the buildout of data centers were up strongly, led by U.S.-based Vertiv, a provider of liquid cooling solutions to optimize server performance, Irish-based commercial HVAC provider Johnson Controls, which is seeing robust order growth among data center customers, as well as Germany’s Siemens Energy, a manufacturer of high-voltage cables to support greater reach of electrical grids.

Health care was also supportive, led by a combination of secular growers as well as more innovative, emerging growth holdings. U.S. pharmaceutical and health care products company Johnson & Johnson benefited from an acceleration in earnings as it moves past a loss of exclusivity on a major drug franchise. U.S. biotech CG Oncology rerated on the announcement of an accelerated timeline for it clinical trial for a new bladder cancer treatment, U.K. biotech Roivant Sciences rose strongly on positive clinical trials for a rare skin disease treatment, while China contract drug development firm Wuxi AppTec was up on strong results and easing tensions with the U.S.

Portfolio Positioning

We continued to diversify our growth exposure into more cyclical as well as emerging growth companies. Among structural growth names, additions included semiconductor equipment maker ASM International and Lasertec. ASM is the leader in atomic layer deposition, a precise deposition technique required in the most advanced semiconductors. The Dutch company’s main clients are logic foundries Taiwan Semiconductor, Samsung and Intel, as well as memory foundries SK Hynix and Micron Technology. Foundries and wafer fab equipment providers like ASM work closely, which gives the firm insight into customers’ innovation and product road maps. Japan’s Lasertec is a pure-play leader in inspection and measurement equipment that is well-positioned to benefit from the emerging growth drivers of extreme ultraviolet (EUV) memory adoption and AI infrastructure. We took advantage of an attractive entry point given that the company is at trough earnings with order recovery ahead. Within the semiconductor complex, we also purchased Japanese medical device and semiconductor products maker HOYA, South Korean memory chip supplier Samsung Electronics, and Taiwanese system-on-chip maker MediaTek.

On the emerging growth side, our purchase of South Korea’s SK Telecom offers participation in a handful of privately held AI enablers through both the company’s internal LLMs as well as minority investments in U.S. LLMs Anthropic and Perplexity.

Among our largest sales were U.K.-based bank NatWest Group, Italy’s Intesa Sanpaolo and U.S. banks JPMorgan Chase and Bank of America. What has historically been positive for financials turned negative for the month — even for banks — primarily on profit taking in the market. While we have reduced our positioning in financials, we remain overweight, primarily in banks. Other sales included Israel’s Check Point Software, which we sold as revenue growth acceleration is taking longer to play out than expected.

We broadly reduced the portfolio’s software exposure, partially through sales of Germany’s SAP and U.S.-based Oracle, as the expansion of AI APIs — tools that allow developers to integrate pretrained AI tools into applications — has intensified competitive pressure across enterprise software models. Concerns around this impact, which began last year, have persisted and increased, with the industry declining more than 20% year to date, significantly underperforming the overall market. This underperformance has not been driven by weakening fundamentals but rather by valuation compression as investors reassess terminal growth assumptions and the durability of traditional software business models in light of accelerating AI innovation.

Outlook

War has changed cost economics around the world, which we know is not good for Europe due to its energy dependence, as we saw during the early stages of the Russia-Ukraine war. How long this lasts and what the result will be has yet to be determined, especially with Iran controlling the Strait of Hormuz, and we must look at potential impacts across several areas. We are analyzing how inflationary pressures from higher commodity prices could impact consumers, as well as what they mean for input prices for industrial and materials companies. We are also watching for a potentially K-shaped U.S. economy where lower-income consumers could struggle from a return of inflation.

We have also been carefully vetting the portfolio to be better in tune with the current risk environment and ensure we are appropriately positioned for the next leg of growth. We have reduced our IT overweight while continuing to add to utilities and materials. We see these structural companies as the new growth stocks and have seen early signs validating our thesis. We have also been moving more meaningfully into Japan, and to a lesser extent Australia, highlighting an overall priority to add in places where we see inexpensive valuations and rising earnings. Often, intensive volatility creates opportunities, and we are looking to add to holdings that have been unduly hit in the broad selloff. Meanwhile, AI disintermediation fears cause us to be intentional and measured in building our AI exposure across our three growth buckets.

Portfolio Highlights

During the first quarter, the ClearBridge Global Growth Strategy underperformed its MSCI ACWI benchmark. On an absolute basis, the Strategy produced positive contributions across two of the nine sectors in which it was invested (out of 11 total): industrials and consumer staples. The IT and financials sectors were the chief detractors.

Relative to benchmark, overall stock selection and sector allocation detracted from performance. In particular, stock selection in IT, financials, communication services and consumer discretionary sectors, an underweight to materials and a lack of exposure to energy weighed on results. On the positive side, stock selection in industrials and health care contributed to performance.

On an individual stock basis, the largest detractors from returns were HDFC Bank in financials, Sea Limited in consumer discretionary, AppLovin and Samsung Electronics in IT and Tencent in communication services. The primary contributors were Vertiv, Siemens Energy and Johnson Controls in industrials as well as Johnson & Johnson and CG Oncology in health care.

Related Perspectives

Navigating Disruption via Infrastructure and Value

Shane Hurst and Grace Su weigh in on how global infrastructure companies as well as value stocks with improving fundamentals help navigate a world marked by disruption from AI, the energy transition and geopolitical tensions.

Read full article