U.S. Equity Outlook: Resilience to Keep Bull Market Intact

Key Takeaways

- Capital spending, bolstered by front-loaded fiscal stimulus, as well as continued consumption by a resilient U.S. consumer, is expected to sustain corporate profit growth at double-digit rates in 2026, leading to positive yet more modest equity returns.

- While AI’s disproportionate role in driving market returns and index concentration shares unhealthy parallels with prior periods of speculation, leading companies today are much more fundamentally sound. We believe a recent pause in investor enthusiasm for the AI trade is also healthy for markets.

- With capitalization-weighted versus equal-weighted S&P 500 Index returns at an extreme and an expected rebound in relative earnings growth for the average stock, we expect a broadening of market participation that should benefit more diversified portfolios in 2026.

Entering 2026 with High Valuations, Elevated Volatility Risk

As we look forward to 2026 it is impossible not to look backward at the last three years of extraordinary returns in U.S. equity markets. The U.S. stock market, as defined by the S&P 500 Index, has risen 78% cumulatively on a three-year basis. While this large advance alone does not inform our view on potential 2026 market returns, both elevated expectations and high valuations make forecasting outcomes particularly challenging next year. On one hand, the antecedent conditions make the market vulnerable to shocks and surprises. Conversely, the current economic momentum bolstered by multiple catalysts could drive an earnings acceleration and broader industry participation in 2026 (Exhibit 1). In our opinion, the most likely outcome is another year of positive, but more modest, stock returns with an elevated risk of market volatility (Exhibit 1).

The most remarkable factor driving markets over the last several years has been the resiliency of economic growth. AI investment, which today is responsible for approximately one-third of all capital investment, as well as continued spending by the U.S. consumer, have sustained S&P 500 profits, which will likely grow again at double-digit rates in 2026. Front-loaded fiscal stimulus from the One Big Beautiful Bill is estimated to add 50-100 basis points to GDP next year and, while there is stimulus for both consumers and corporates from the bill, businesses will be able to immediately deduct capital expenses such as investments in equipment and R&D. This is expected to bolster overall capital spending, which should broaden and remain strong even if AI capex spending moderates in 2027 and beyond.

However, as we look forward to next year, we think job creation could pick up to 80,000 or 90,000 per month on the back of Fed cuts, the peak fiscal impulse of the One Big Beautiful Bill (OBBB) and more visibility on the tariff front once we get the Supreme Court’s decision on the legality of the International Emergency Economic Powers Act (IEEPA) tariffs. Although this is lower than the past several years, it is certainly enough to keep this expansion moving forward.

Exhibit 1: Closing the Gap

The term “consensus” within the capital markets industry refers to the average of earnings estimates made by professionals. Magnificent 7 data refers to the following set of stocks: Microsoft (MSFT), Amazon (AMZN), Meta (META), Apple (AAPL), Google parent Alphabet (GOOGL), Nvidia (NVDA), and Tesla (TSLA). Data as of Nov. 30, 2025. Sources: FactSet, S&P.

With inflation forecast to remain notably above the Fed’s 2% target and a higher than commonly understood neutral rate, we believe rates will be cut by less than consensus expects in 2026.

The consumer calculus is a bit more mixed, but here again resiliency is our expectation. Confidence and spending data show a clear divergence between the low- and high-end consumer. Employment is the key ingredient for consumer health, but the current weakness in labor demand is also partly a reflection of shifts from immigration, as well as a lower need for labor hoarding, which originated during the COVID years and kept unemployment levels at unusually tight and perhaps unsustainable levels. We believe that labor pressures from AI, as well as benefits from AI productivity, while very real in specific circumstances, are likely overstated in terms of their current impact on the broader economy.

Monetary policy should also provide a tailwind to the economy although, in our view, to a lesser degree than the market believes as long-dated yields could remain high with some risk to the upside. Fortunately, the impact of tariffs, both on supply chains and inflation, has been less inflationary than feared as distributors and manufacturers have been willing to absorb some of the impact. Overall, the effective tariff rate is projected to settle in the 6%–8% range, less than half the assumed rate six months ago, due to a bevy of carve-outs and exemptions that have mitigated the impact.

That said, some consumer-facing segments of the economy are clearly experiencing pricing pressure. Fortunately, continued disinflationary trends in housing and energy are likely to provide at least a partial offset. Our view is that with inflation forecast to remain notably above the Fed’s 2% target and a higher than commonly understood neutral rate, federal-funds rates will be cut by less than consensus expects in 2026. Furthermore, a potential re-acceleration in economic growth, real worries about the politicalization of the Federal Reserve, and an increase in fixed income supply from both growing deficits and AI financing requirements all have the potential to drive yields higher.

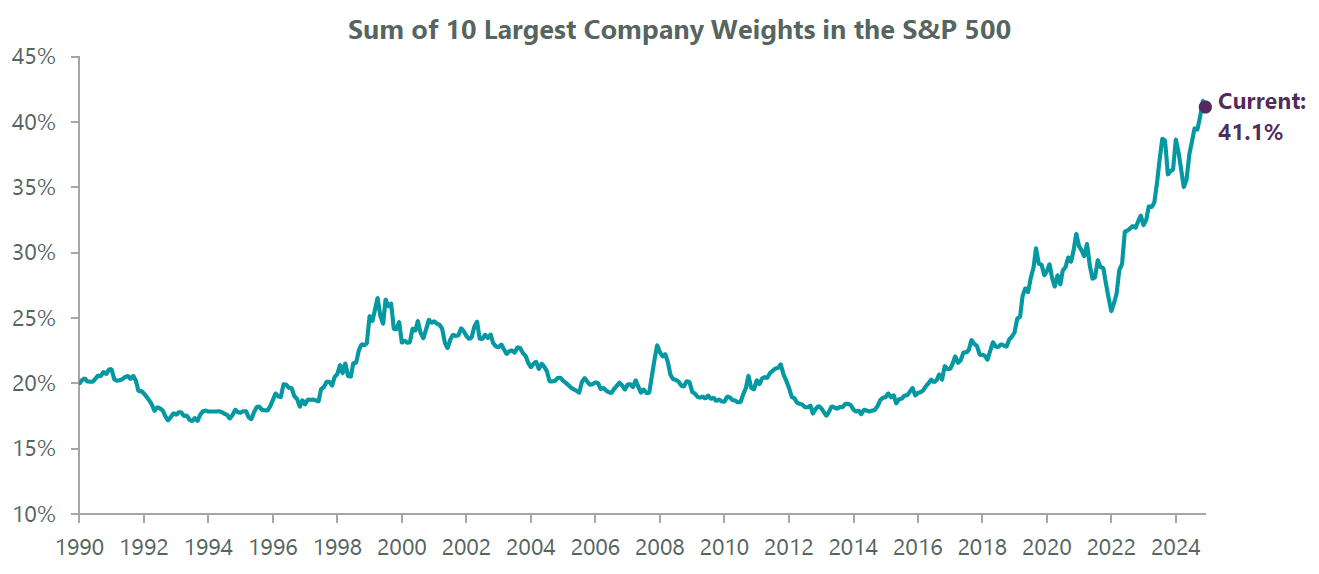

Exhibit 2: AI Enthusiasm Has Amplified Market Concentration

Data as of Nov. 30, 2025. Sources: S&P, FactSet, and Bloomberg.

Finally, we have some concerns over the disproportionate role AI is playing in driving overall market returns and its resulting effect on market index concentration (Exhibit 2). From both our studies of historical market bubbles, as well as from our own experience as investors over the last 30 plus years, we see some unhealthy parallels with prior periods. These include extreme valuations, circular financing arrangements, a surge in retail participation and increased speculation, particularly through leveraged ETFs and single-day options.

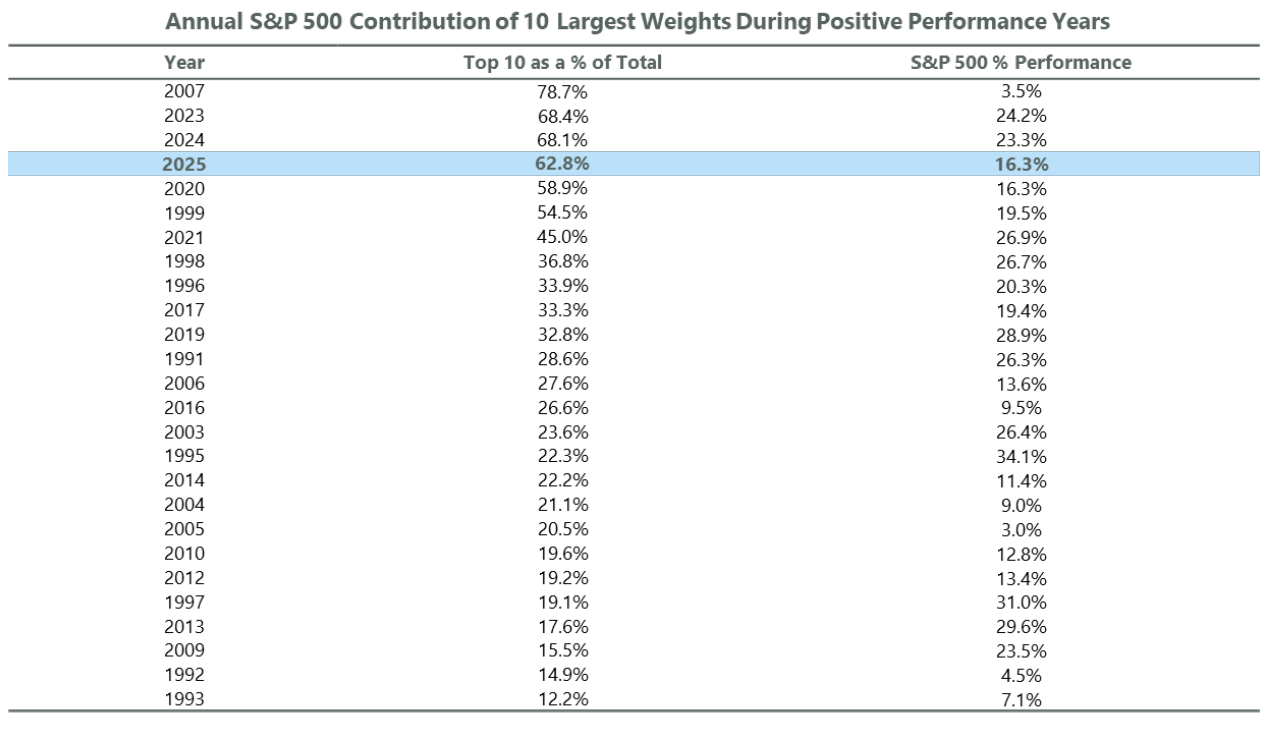

Exhibit 3: Largest Stocks Have Driven Performance in Current Era

As of Oct. 31, 2025. Source: Strategas, Bloomberg.

That said, there are several distinct differences from the tech bubble of the late 1990s and early 2000s, with today’s leading companies funding much of their investment into new technology from free cash flow. When external capital does need to be raised, it is largely being done from sticky sources such as debt or private markets. This stands in contrast to the tech bubble when leading companies did not generate profits or free cash flow and relied on equity financing (IPOs and secondaries). While pockets of speculation are apparent today, they bear little resemblance to the breadth of speculation seen 25 years ago, suggesting more limited contagion risk.

The AI narrative is changing, with the winners and losers at this stage harder to identify and needing a seemingly endless supply of cash. Importantly, investors are starting to question the financial returns that this investment will ultimately produce, which has led to market volatility such as what occurred following the release of DeepSeek’s lower-cost high-performance R1 model in January 2025. AI will no doubt change the world and have profound effects on business efficiency and consumers’ lives; however, the path for new technologies is rarely without twists and turns and often takes longer than anticipated. We believe the recent pause in enthusiasm is healthy for the overall market as it tempers the risky “bubble” parallels highlighted earlier and increases the odds for more balanced equity returns next year.

With capitalization-weighted versus equal-weighted S&P 500 Index returns at an extreme and an expected rebound in relative earnings growth for the average stock, we expect a broadening of market participation that should benefit more diversified portfolios in 2026.

Related Perspectives

2026 Australian Equity Outlook

Explore the dynamic landscape that Australian Equities experienced over 2025, prospects for the market, and ClearBridge Australian Active Equity and Equity Income portfolios in 2026.

Read full article