Selective about infrastructure

The case for a specialist approach

The listed infrastructure sector is notable for providing income and lower long-

term volatility. However, it’s important to recognize that not every stock in this

sector contributes equally to that goal.

Listed infrastructure has been shown to be a sector where investors can find defensive growth. Notably, the major listed infrastructure indices* tend to perform defensively against global equities.

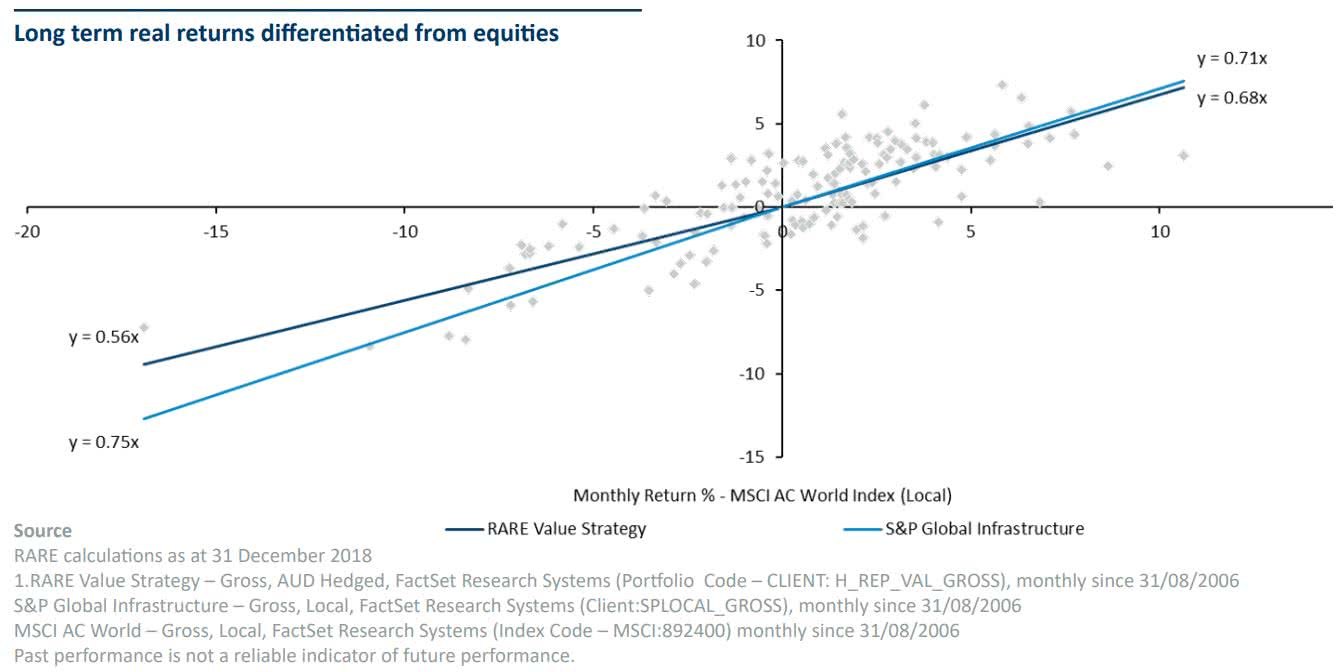

Consider the chart below. The light blue line illustrates the monthly performance of the S&P Global Infrastructure Index over the past 13 years against the MSCI AC World Index. It shows that the S&P Global Infrastructure Index participates in around 70-75% of the volatility of global equities both in months when markets rise as well as when they fall – in other words it displays lower beta to global equities.

So, it can be seen that a generalist approach to listed infrastructure offers a measure of protection. However, the dark blue line in the chart shows the application of a more selective approach to listed infrastructure as carried out by the RARE Infrastructure Value Strategy. This has brought much greater downside protection, while only sacrificing a small amount of the upside of a generalist approach.

The reason for the difference in outcomes is driven by two factors:

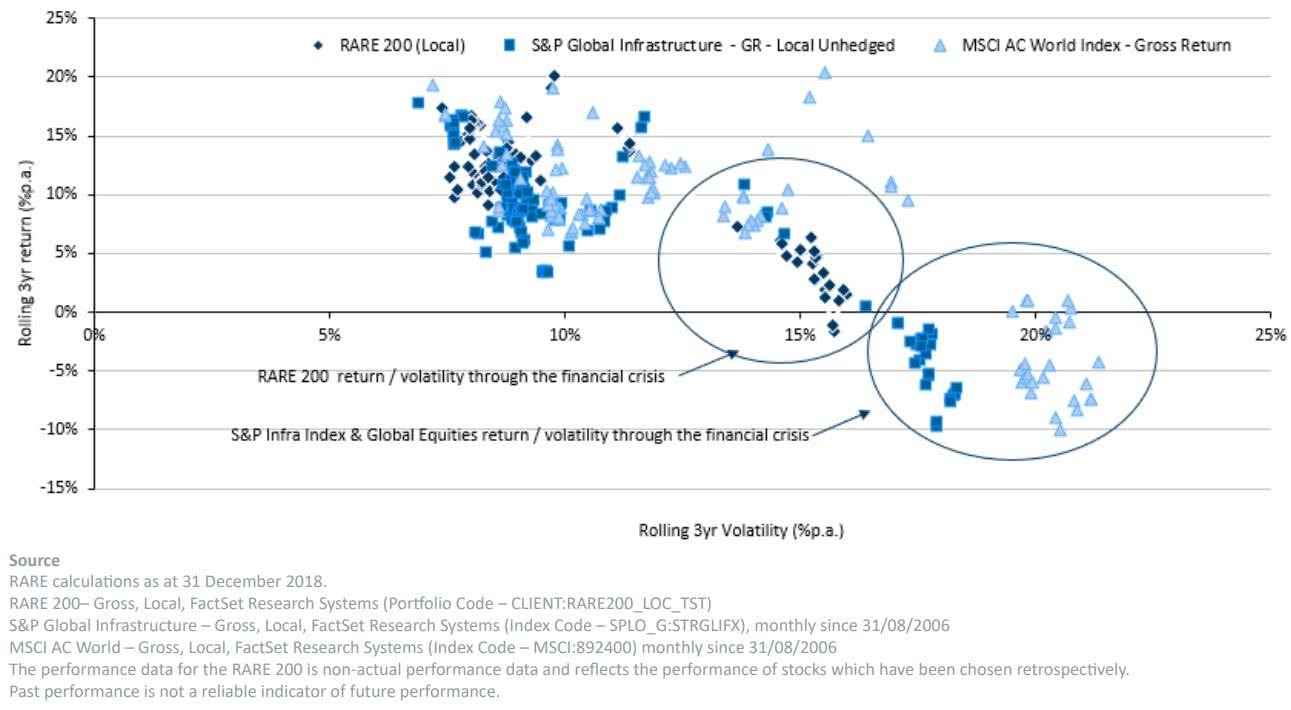

1. The definition of infrastructure. Listed infrastructure indices cover a range of companies that vary greatly in their nature – not all of which are conducive to defensive growth. Some firms own assets that command the most desirable attributes of the sector – pricing power, limited competition and inflation-linked revenues. Most indices also include companies that lack these attributes – such as companies highly exposed to commodity prices; utility retailers and telecommunications companies that compete with each other for market share; and service, logistics and maintenance companies that do not own hard assets. The chart below illustrates that while during more benign markets it may be difficult to tell these approaches apart, the definition of listed infrastructure can provide an important source of protection in down markets. During the last severe downturn (GFC) the RARE200, the investment universe for the RARE Infrastructure Value Fund, delivered an improved risk and return profile than the S&P Global Listed Infrastructure Index which performed only marginally better than global equities.

2. Benchmark unaware portfolio construction. RARE’s approach targets an absolute return benchmark over rolling 5-year periods. Portfolio construction guidelines allow the Portfolio Managers the flexibility to allocate between the more defensive, regulated utility sectors, and the more economically sensitive user pays assets. The ability to rotate the portfolio through economic cycles has led to the Value Strategy improving on the downside results when compared to the RARE200 without material impact on the upside.

Core infrastructure defined

We believe investors who seek defensive growth and/or higher-than-average premiums are better served focusing on “core” listed infrastructure companies – RARE defines this criteria as follows:

-

Predictable cash flows: Regulation and/or long-term contracts which enforce viable and stable cash flows can result in a relatively stable source of earning and dividend income.

-

Low volatility valuation: Firms with predictable and stable revenues, cost structure and capital expenditures are less likely to have a volatile market valuation.

-

Inflation protection: Infrastructure revenue is often linked to inflation, whether due to regulation, concession agreements or public contracts.

-

Long-duration assets: These are long dated income generating assets, with a revenue stream that often occurs over a number of decades.

-

High barriers to entry: The size and expense of most infrastructure assets means that, by design, they often operate as monopolies or oligopolies. This market power tends to lead towards lower volatility in the market price due to the stability in market pricing and cash flows.

Building a listed infrastructure portfolio

Once these requirements for companies are met, infrastructure strategies can be better tailored to pursue specific outcomes.

If an investor is particularly risk averse, portfolios can lean toward companies that offer essential services such as water, electricity and gas. Demand for these remains relatively stable even in times of economic weakness, making the revenue of utilities easier to project.

If the economic outlook is more positive and investors are prepared to take higher risks, then an infrastructure portfolio should have a higher proportion of ‘user pay’ assets. Railways, airports, roads, ports, mobile phone towers and satellites are examples of user pay assets, all of which are critical to move people, goods and services through an economy. These assets generally offer high barriers to entry and therefore have defensive properties. However, as an economy expands, their revenues also typically grow – giving them a growth component.

A portfolio that dynamically allocates to both types of infrastructure in response to valuation opportunities and shifts in economic outlooks has the potential to get the best of both worlds.

Fine tuning the portfolio

The investor can choose to be overweight to emerging market listed infrastructure. When blended into a global portfolio, carefully selected emerging market stocks can offer higher potential dividends owing to higher rates of interest in most EM countries. They also help diversify risk and widen the opportunity set, giving the potential for greater risk-adjusted returns.

Conclusion

In building a defensive growth portfolio, we believe in strict entry requirements for the companies. Simply because a company is categorised as being in the infrastructure sector does not make it part of the solution. Companies should be analysed to see if they meet the hurdles of having predictable cash flows, inflation protection, owning long-duration assets and having high barriers to entry and limited competition in their market

Related Perspectives

Global Infrastructure Income Strategy Commentary Q2 2026

Infrastructure Positive but Trails in Risk-On Quarter

Listed infrastructure made positive gains, led by user-pays assets such as airports and rail in a risk-on environment of easing geopolitical tensions.