Infrastructure Outlook in 2022: Defensive Growth, or Just Defense?

Key Takeaways

- In an uncertain macroeconomic environment, the certainty of future earnings and growth will be key: infrastructure and utilities significantly outperform other equities on this measure.

- Given our base case of slowing growth and higher inflation, our playbook for infrastructure portfolios broadly is to watch for a transition from a growth orientation to a more defensive positioning as growth fades and utility underperformance unwinds.

- Generally, user-pays infrastructure and utility returns are positively correlated to inflation, but results differ by sector and region; meanwhile, climate inflation looms and is underappreciated at present.

Inflation and Growth Slow in 2022, but How and When?

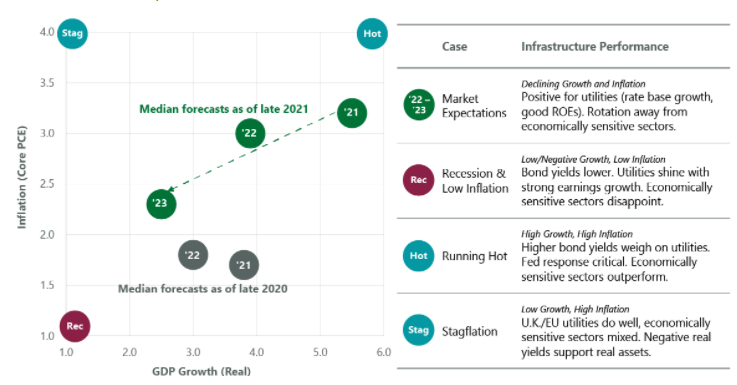

The surprises over the last 12 months should give some indication of the significant uncertainty facing investors in 2022, with forecasts for global GDP growth and inflation having a high chance of coming in well above or below consensus. Market expectations for 2022 have moved significantly in recent months, on the whole pointing to a hotter than expected economy (Exhibit 1: gray dots are expectations as of late 2020, green dots as of late 2021). Broadly, markets expect gently slowing inflation and growth over the 2021–23 period (the green dots move progressively to the lower left corner for 2021, 2022 and 2023). The question will be how much and when.

With supply chain issues, higher housing costs, higher commodity prices and producer price inflation remaining square in the sights for 2022, we think higher inflation is a risk for global markets. We expect growth to slow to trend or below by mid-2022 and U.S. Treasury yields to rise, which will mean a continuation of negative real bond yields. Additional forecast volatility and therefore market uncertainty will arise as new COVID-19 variants appear and circulate. However, with high levels of vaccination across the developed world and less propensity for mobility restrictions and lockdowns, we expect the economic implications to be limited.

Exhibit 1: Market Expects Slower Growth and Inflation

As of Nov. 30, 2020 (gray color), and Nov. 30, 2021 (green color). Source: ClearBridge Investments, Bloomberg Finance LP. Forecasts may not be met. Opinions may change at any time without notice.

Rising bond yields are relatively more important for longer-duration assets. Within infrastructure, utilities tend to be shorter duration (as their assets are repriced by regulated returns at frequent regulatory resets, making them relatively less sensitive to movements in bond yields over the medium term), whereas toll road and concession assets without the ability to reprice their assets or returns tend to be longer duration and hence relatively more sensitive to changes in interest rates. We expect nominal bond yields to remain relatively low by historic standards for the long foreseeable future; this means real yields will remain negative and continue to support investment in infrastructure.

- Utilities, generally the defensive play, performed poorly early in 2021 amid a sharp cyclical rally and have traded sideways since. Electricity, gas and water companies have continued to invest in their asset bases and regulators have continued to provide attractive returns (8%–11% nominal ROE), resulting in highly predictable earnings growth over multiyear horizons. However, expectations of rising bond yields (particularly real yields) continue to weigh on the sector, and traditionally utilities have lagged the market until the first rate hike is announced and the path of rate hikes becomes more certain. As a result, utilities could lag for the first half of 2022.

- Transportation infrastructure generally offered a mixed bag in 2021: toll roads recovered quickly from the initial stages of the pandemic and did well amid subsequent waves of COVID-19 as people decided against public transport and commuted in cars. Airports remain challenged as additional lockdowns loom. Ports and rails have lagged as snarled supply chains have reduced utilisation and volumes. Transportation infrastructure should see a strong start to 2022 as growth returns to the economy and supply chain constraints ease (likely over the course of the year).

- Communications infrastructure such as tower companies struggled in 2021. We expect communications to perform well in 2022 on continued negative real rates and high growth, driven by increased bandwidth needs as 5G buildout increases. The 5G network buildout will continue at pace in 2022 and beyond as users (mobile handsets) increase in number and data continues to trend higher with more macro and micro sites required. This will support 5G network speeds; however, more work is required to reduced latency.

- After a strong 2020, renewables had a poor 2021 until the runup to COP26 as focus returned to the enormous policy support for renewable energy. The passing of the U.S. infrastructure bill and ongoing revisions of global emission reductions targets supports renewables, so we expect the sector to carry strength into 2022. Higher fossil fuel prices will assist the transition to renewable energy as projects that were marginal become economically justifiable.

- Energy infrastructure, while generally not directly correlated to energy prices, benefits from future growth in production activity. The development of gathering networks and gas and liquids transportation provides ample opportunity for investment and attractive returns in a world of higher energy prices. Meanwhile investments in green hydrogen and carbon sequestration activities may assuage those investors concerned about the long-term viability of these (largely and currently) fossil-fuel-focused networks.

Against this backdrop, given our base case of slowing growth and higher inflation, our playbook for infrastructure portfolios broadly is to watch for a transition from a growth orientation, in which we prefer higher exposure to economically sensitive user-pays infrastructure and lower utility weightings, to a more defensive positioning as growth fades and utility underperformance unwinds. In the base case economic view this will be a measured process throughout 2022, while in the alternate view this transition will be accelerated. We’ll look for defensive growth exposure through communications and high-growth utilities, including renewables, and we’ll look to ensure strong inflation correlation with utility positions, including the use of midstream pipelines that would benefit from a structural change in the view of long-term equilibrium energy prices.

A Multiple/Margin Conundrum

Overall, markets will find support given excess liquidity, but should be subject to corrections as growth and inflation expectations are recalibrated. We expect markets to be broadly in a mid-cycle phase, where earnings growth is required to support multiples and returns moderate from the relatively high levels of the last three years. Consumer price inflation is running in the mid-single digits and is likely to continue well into 2022. Meanwhile, producer price inflation is running in the low double digits and is also likely to continue well into 2022. This sets up an interesting conundrum: companies will have the option to pass on the increased input prices (producer price inflation) to finished goods. This should ramp up inflation and rates expectations as well as bond yields, leading the cost of capital to increase and earnings multiples (and therefore stock prices) to decrease. Alternately, they can absorb the increased input prices, which would lead margins and earnings (and therefore stock prices) to decrease.

Going forward, in an uncertain macroeconomic environment, the certainty of future earnings and growth will be key: infrastructure and utilities significantly outperform other equities on this measure, with the impact of the pandemic and large trends such as decarbonisation in the face of climate change either largely known or highly predictable.

Inflation and Infrastructure Assets

Uniting our base case and alternate views is higher inflation, and we have written extensively about how inflation is generally a pass-through for infrastructure assets. Generally, user-pays infrastructure and utility returns are positively correlated to inflation, but results differ by sector and region. Some sectors have a direct link to inflation: utilities in the U.K., parts of Europe and Australasia have returns and often asset bases indexed to inflation annually. Utilities in the U.K. and Europe should do well in a low-growth, high-inflation scenario as their earnings certainty and direct inflation pass-through will look attractive. Toll roads have earnings rates indexed to inflation on a quarterly or annual basis. Airports will often have inflation-indexed retail leases and regulatory regimes for aeronautical activities.

Sectors with indirect links to inflation include utilities regulated on a nominal basis, as in North America and parts of Europe, where the utility commissions generally provide an allowed return based on a nominal return on equity (ROE) invested in their asset bases. There the inflation pass-through may lag as the ROE, capital structure and costs are adjusted when the utility files for its rate case. Pipelines include regulated and commercial activities; while there is inflation pass-through for the regulated component of the business, the level and speed of inflation pass-through for the commercial activities depends on the nature of the contracts underpinning those activities.

Should inflation persist as we believe it will, infrastructure portfolios will hinge mainly on what type of growth we see: amid lower growth, we would look to add utilities, with bond yields lower and utilities not sensitive to a downswing in GDP. If growth surprises to the upside, transport infrastructure, in particular toll roads, will look attractive as higher GDP would result in higher economic activity and higher throughput.

The Other Inflation: Climate Inflation

Once pandemic-related supply inflation begins to fade, looming not too far off is climate inflation, which remains a relatively underdiscussed issue. We expect climate inflation to begin to appear in the middle of this decade and likely run for a decade or two. There are several drivers for this: carbon pricing will be critical to delivering market-based decarbonisation, even while this likely leads to higher prices for everything in the medium and long term. For example, the EU Fit for 55 program will implement a carbon border adjustment mechanism, which will result in carbon being priced into goods (across a range of industries) sold in Europe and may result in a decade of rising prices. Among renewables, project build costs are now starting to rise because of rising commodity costs (copper particularly). Additionally, the nature of renewable energy generation will require significant additional electric transmission lines and additional generation to offset the interruptible nature of renewables. Fossil fuel energy sources should have higher breakeven prices in the future as fossil fuel projects will likely have higher costs of capital associated with them (due to fewer sources of capital as banks move away from fossil fuel lending) and capital will likely need to be recovered over shorter time periods. Utilities are not without their climate-related expenses either: the New York City sewer system, for example was built to handle 1.75 inches of rain per hour. During Hurricane Ida the city got over 3 inches in an hour. It will cost $100 billion to recalibrate the system and take several decades. That cost will be recovered in utility bills.

The U.S. Infrastructure Act

Finally, the most significant element for private capital from the recent $1.2 trillion Infrastructure Investment and Jobs Act will likely be the provisions streamlining permitting processes, particularly for electric transmission lines. These lines, for which we have seen permitting processes as long as five years, are often the missing link as we build out a grid for an electric future. Electric transmission is critical for the U.S.’s emissions goals — a Princeton University study last year concluded that the U.S. needs to increase the electric transmission network by 60% (in terms of gigawatt miles of wires) by 2030 in order to hit its net-zero by 2050 target.

A Quick Word on Valuations

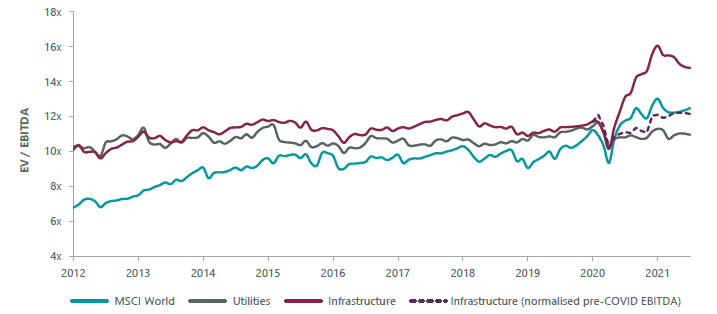

Infrastructure looks attractive from a valuation perspective. A common earnings multiple metric for global utilities and user-pays infrastructure (enterprise value to EBITDA, earnings before interest tax depreciation and amortisation) has traded in the 10x–12x range since 2012, adjusting the earnings of infrastructure companies, particularly airports and passenger rail networks, for the impact of the pandemic (Exhibit 2).

Exhibit 2: Utility and User-Pays Infrastructure Consensus EV/EBITDA

As of June 30, 2021. Source: ClearBridge Investments and FactSet Research Systems. Arithmetic average, current EV divided forward consensus EBITDA (or, if not available, internal forecasts). EV = market cap + net debt + minority interest and preferred stock. EBITDA = earnings before interest, tax, depreciation and amortisation.

Yet over the last decade we have seen a steady decline in the cost of capital for utility and infrastructure companies, combined with an increase in forward earnings growth, particularly in the utility sector that is investing in its asset base to decarbonise economies and mitigate the effects of climate change. We believe the market has not taken into account the cheaper cost of capital and better growth profile for these sectors. Based on this disconnect, we believe there is room to run for infrastructure in 2022.

Related Perspectives

Global Infrastructure Income Strategy Commentary Q2 2026

Infrastructure Positive but Trails in Risk-On Quarter

Listed infrastructure made positive gains, led by user-pays assets such as airports and rail in a risk-on environment of easing geopolitical tensions.