Inflation and Higher Rates: What They Mean for Infrastructure

Key Takeaways

- Energy-driven inflation and geopolitical risk increase the likelihood of higher-for-longer interest rates.

- Many infrastructure cash flows have built-in inflation pass-through, which can help protect real returns over the medium to long term.

- Inflation sensitivity varies by asset type: regulated utilities tend to adjust returns over time as regulators reset allowed returns, while user-pays and contracted assets depend more on concession terms, contract escalators and demand exposure.

The escalating conflict in the Middle East has increased the risk of energy-driven inflation and raised the prospects of higher interest rate pressures globally. It is difficult to predict both the duration of the war in Iran and the knock-on effects on global energy markets as supply chain disruptions raise oil prices. Central banks such as the European Central Bank and the U.S. Federal Reserve have linked the war to higher inflation and raised concerns of delayed rate cuts or even the need for rate hikes.

How is global infrastructure, typically owned for its income, positioned in a higher-inflation environment?

The impact of higher inflation and rates on listed infrastructure depends on the reason for the increase. It also depends on the type of asset. We distinguish between:

- Regulated assets, where revenues are normally determined by a return on an underlying asset base, which is in turn determined by the level of investment. While the details of how returns are set vary widely between assets, the main difference relates to whether prices and assets are index linked with cash returns based on a real cost of capital (e.g., U.K., Australia), or whether regulators look at nominal assets and grant a nominal return.

- User-pays assets, where control of prices for transport assets is usually set out in a concession contract, with volume risk borne by the operator. Other infrastructure (e.g., communications) often has long-term contracts that include price escalation.

Regulated Assets

One of the most important characteristics of regulated assets is that regulators determine returns based on perceptions of how interest rates and the cost of capital will develop in the future. If interest rates rise, regulators need to increase allowed returns to facilitate future funding of capital investment. Such increases do not happen immediately, but over the medium term regulated returns should rise and fall in line with changes in the cost of capital.

In countries with regular price resets (e.g., the U.K.), regulators review the cost of capital during each price control period. In countries such as the U.S. and Canada, companies apply for permission to increase rates and regulators assess appropriate cost of capital during proceedings.

The legal framework supporting utilities typically requires regulators to offer reasonable returns. As a result, changes in interest rates are reflected in future cash flows over the medium to longer term. Short-term changes, however, can impact valuations depending on the timing of regulatory adjustments.

User-Pays Assets

User-pays assets behave differently from regulated utilities in that they typically have greater exposure to GDP growth. Cash flows increase during cyclical upswings, and long-term cash flows may not immediately respond to changes in interest rates. The behavior also depends on whether returns are linked to inflation indexes. For toll roads, for example, inflation indexation frameworks differ across regions: concessions in the U.K., France, Italy, Spain, Australia and Canada tend to incorporate robust, formula-based inflation linkage with tolls growing at the higher of CPI or a contracted minimum amount. In the U.S., Germany, the Netherlands and the Nordics, concessions still contain essential mechanisms that allow inflation pass-through, though on a more measured basis.

Case Study 1: European Utilities

While regulations in different countries in Europe have various technical differences, in essence they are designed to protect the remunerations utilities receive for capital investment against macroeconomic changes, which include inflation. Nonetheless, there is one major difference within the sector: whether allowed returns (i.e., the weighted average cost of capital or WACC) are set in nominal terms (as in Spain or Portugal) or real terms (as in the U.K. or Italy).

WACC and Allowed Returns Set in Nominal Terms

If the WACC is set in nominal terms, the regulated asset base (RAB) and total capital and operating expenditure allowances are quoted by the regulator in nominal terms. As a result, annual fluctuations in inflation have no impact on the allowed revenue.

Companies with WACC and allowed returns set in nominal terms are viewed as beneficiaries of low inflation: if inflation stays depressed, asset owners may be overcompensated in the regulated cash flows to cover cost inflation in capital and operating expenditures (due to allowances set in nominal terms), and vice versa, during the period.

However, the lower nominal bond yields resulting from a low inflation rate would be factored into the regulator’s return allowance in the next WACC review, and vice versa. For instance, for electricity networks in Spain, the WACC allowance is set as nominal for the new regulatory period 2026–31, with reference to prior and forecast inflation. As such, allowed returns allow for the pass-through of actual inflation, albeit with a time lag of a few years.

WACC and Allowed Returns Set in Real Terms

If the WACC is set in real terms, parameters such as RAB and total capital and operating expenditures are typically estimated and approved by the regulator in real terms using forecast inflation for any regulatory period. The returns permitted by the regulator (allowed returns) are then adjusted annually by actual inflation when determining the regulatory cash flow and asset base, i.e., they are passed through to the customer through higher rates, at times with a lag of a few months. Consequently, if inflation trends higher than the regulator’s forecast before the start of the period, there is a momentary boost to the cash flow compensation, and vice versa.

Companies with WACC and allowed returns set in real terms are viewed as beneficiaries of high inflation.

However, taking a more holistic view over the regulatory period, if inflation remains high for several years, it is taken into consideration by the regulator’s assumption heading into the next price review, thereby driving down the real bond rate allowance embedded in the allowed return. The impact on the asset cash flows from inflation-related drivers gets averaged out over the long term. In addition, companies may have mechanisms to further moderate the sensitivity to inflation, such as using inflation-linked bonds as part of their borrowings.

The higher the proportion of debt being inflation-linked, the more muted the short-term effects from inflation shocks are on the cash flows.

Case Study 2: North American Utilities

Fundamentally, North American utilities are relatively insulated from changes in inflation because customer rates are set under a cost-of-service regulatory framework. Under this model, utilities are permitted to earn a return on their invested capital (for example an electric utility’s investment in poles and wires), and to recover prudently incurred operating expenses (such as maintenance, taxes and fuel, etc.), subject to regulatory approval. When costs rise, utilities can file a rate case or use established adjustment mechanisms to customer bills with higher expenses. While the timing of recovery can vary, over the medium to longer term utilities generally increase rates in line with changes in underlying costs.

One area where inflation may influence utilities is in the determination of allowed returns. Assuming real interest rates remain unchanged, higher inflation typically leads to higher nominal interest rates, which regulators often reference when setting a utility’s allowed return on equity (ROE).

In some jurisdictions, allowed ROEs are formulaically linked to specific interest rate benchmarks and adjust automatically within defined parameters. In California, for example, allowed returns are annually adjusted when utility bond yields, referencing data from Moody’s, change by more than 100 bps.

In other states, returns are determined through periodic rate cases, where capital market conditions form part of the assessment. In both approaches, regulators seek to provide returns that are sufficient to attract capital while balancing customer affordability.

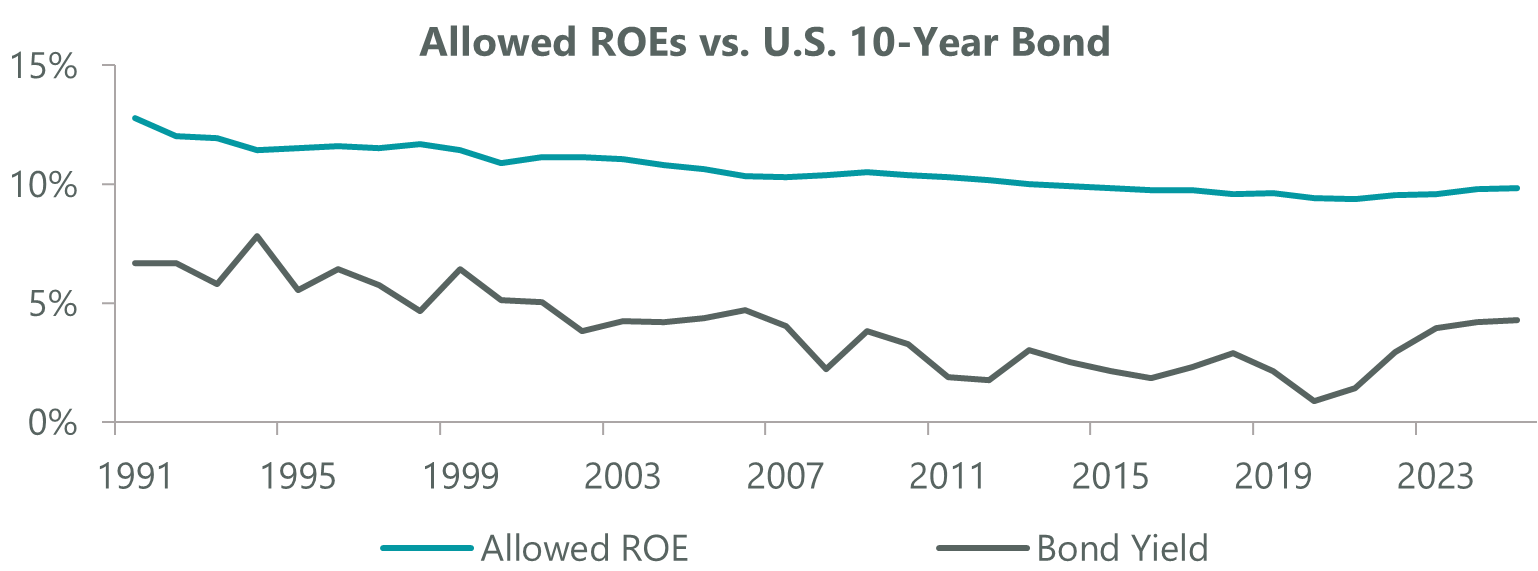

Historically, allowed ROEs tend to adjust gradually rather than immediately in response to changes in bond yields (Exhibit 1). Regulators typically prioritize stability and may wait for sustained shifts in capital market conditions before revising returns. As a result, movements in interest rates are generally reflected in allowed ROEs over time rather than on a one-for-one basis in the short term.

Overall, while inflation and interest rate changes can create near-term valuation volatility due to the regulatory lag and capital market movements, the cost-of-service framework is designed to allow recovery of operating and capital costs over time. Provided regulatory systems remain constructive, inflation is typically passed through directly or indirectly, limiting its impact on long-term cash flows.

NextEra Energy (NEE) provides a current example of how the cost-of-service framework supports inflation pass-through over time. At its regulated utility, Florida Power & Light, a recently approved rate case includes a 10.95% allowed ROE (increased from 10.8%), $2.2 billion of base rate increases through 2029 and a rate stabilization mechanism that supports earnings visibility and the ability to defer future rate cases. The inclusion of a large load tariff for data centers further highlights how incremental capital investment and cost increases can be incorporated into rates over time.

Exhibit 1: Allowed Returns Slow to Adjust

As of March 19, 2026. Source: ClearBridge Investments, Bloomberg Finance.

Case Study 3: North American Pipelines

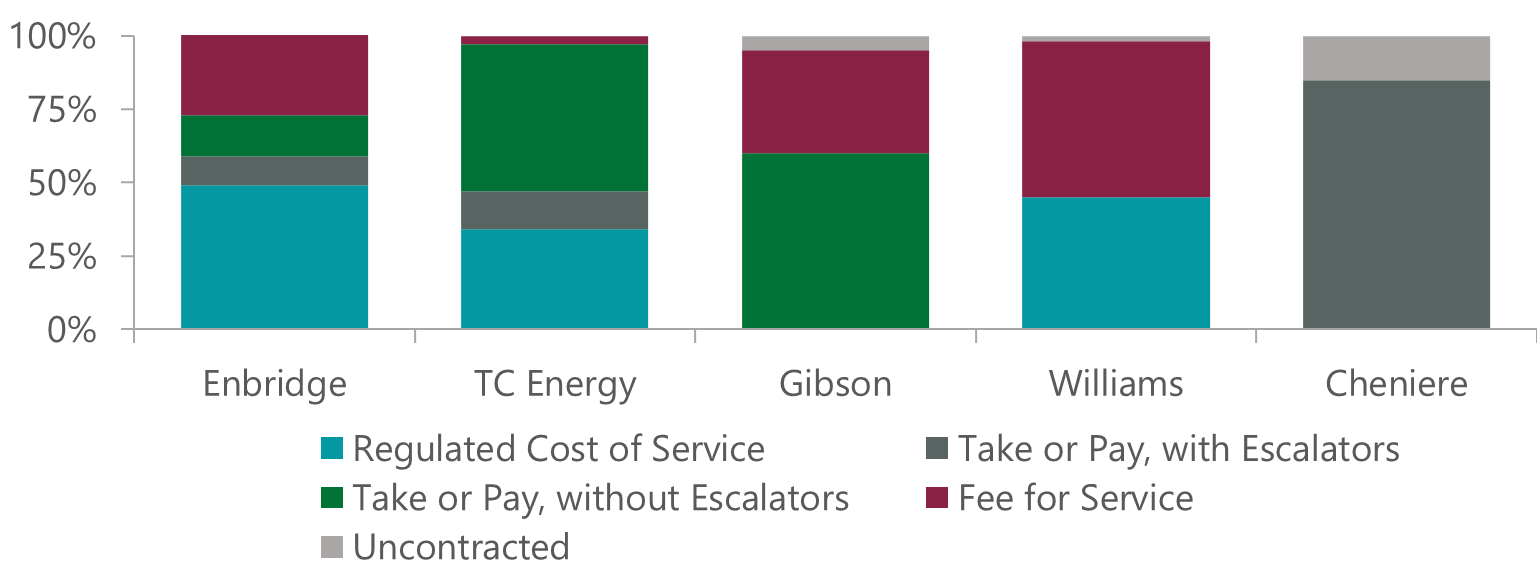

In the case of North American midstream pipelines, the impact of inflation varies depending on the nature of the commercial agreement that underpins pipeline assets (Exhibit 2).

Exhibit 2: Commercial Underpinning of Pipeline Assets

As of March 19, 2026. Source: ClearBridge Investments.

Pipeline companies that operate long-haul transmission networks tend to have the highest level of inflation protection as they operate under a cost-of-service methodology or have long-term take-or-pay contracts with annual escalators embedded in their terms. For example, Enbridge’s Lakehead System (the U.S. portion of the Liquids Mainline System), has rates that are either indexed to PPI or cost-of-service, while the Canadian Mainline (the Canadian portion of the Liquids Mainline System) has tariffs that are a function of GDP.

Enbridge’s gas transmission assets have recently gone through a rate case to redetermine rates to reflect cost inflation, among other items, which resulted in an earnings uplift. Those midstream assets that work under a fixed-fee take-or-pay contract (such as Gibson Energy’s oil sands storage tanks) or fee-for-service model (such as Williams’s gathering and processing infrastructure) are more exposed to inflation.

To the extent that higher inflation is a product of higher commodity prices, that would generally be positive for midstream companies as:

- Higher commodity prices mean healthier E&P counterparties/customers.

- Higher prices may lead to more E&P activity, which may mean more infrastructure/growth capex is required.

- Midstream companies that have non-contracted volumes/marketing arms benefit directly by selling product at higher prices.

Case Study 4: North American Renewables

Overall inflationary forces have muted valuation impact on global renewables. While renewables companies are largely being compensated through 10-year–20-year fixed power purchase prices or partially inflating agreements, the returns assumed within these agreements tend to have long-term inflation assumptions embedded. Essentially, this means that while there is no explicit pass-through of inflation through the pricing, a pass-through is implicit when the contract is written, and often the contract will contain buffers for rising inflation. For example, renewables companies secure growth from their development pipelines, where fixed-price contracts for the operational stage of assets are negotiated based on current market conditions.

Meanwhile, technology is driving cost deflation, preserving or expanding margins for renewables companies. Automation and software are translating to declining operations and maintenance costs (the largest contributors to costs), which companies broadly expect to continue. Bloomberg New Energy Finance forecasts capital costs in renewable energy to continue to come down through 2050. For example, solar photovoltaics are expected to see an annualized 3% decline through 2040.

Case Study 5: Toll Roads

Rights to operate toll roads are typically granted under a concession and as such usually have a finite life. Concession deeds define the parameters under which the toll road may operate, and, in most cases, this stipulates how toll prices may be increased. Generally, toll price increases are linked to inflation; however, there are a number of variations, including:

- Full inflation pass-through (e.g., the Westlink M7 in Sydney)

- Partial inflation pass-through (e.g., main French and Italian toll roads’ usual 0.7x CPI)

- Inflation pass-through with a floor (e.g., WestConnex in Sydney has greater of CPI or 4% until 2040)

- No inflation linkage (e.g., 407 ETR in Toronto and I-95 in Virginia are free to set tolls subject to constraints)

A toll road company like Transurban can have different escalation mechanisms even within one country. In Sydney, tolls escalate quarterly by Australian quarterly CPI. In Melbourne, they escalate by 1.05% per quarter, the equivalent of 4.25% per year; beginning in July 2029, they will escalate quarterly by Australian CPI. In Brisbane tolls escalate annually by Brisbane CPI. Tolls for the WestConnex tunnel in Sydney escalate annually by the greater of Australian CPI or 4% to December 2040.

The differences in inflation pass-throughs outlined above tend to drive the following outcomes:

- Full inflation pass-through will likely lead to limited sensitivity.

- Partial inflation pass-through will lead to increased sensitivity, albeit costs are typically fixed and increase with inflation, providing for improving EBITDA margins with traffic growth (historically, this is why partial inflation pass-through exists, as inflation is achieved after costs).

- Floor price increases mean valuations are sensitive below the inflation floor. When inflation is decreasing, valuation increases and vice versa.

- Concessions with no inflation linkage will typically mean valuations are affected more by traffic congestion and thus economic conditions.

As such, inflation is typically passed through, making toll road valuations less sensitive to nominal bond rate changes where this is driven by increases in inflation. Toll road valuations are, however, very sensitive to changes in real bond rates without an increase in inflation, thus increasing discount rates without the benefit of inflation-driven increases in cash flows. It is also worth noting that, often, inflation occurs at times of increased economic activity, which typically results in increased traffic levels, further offsetting impacts of inflation from a valuation perspective.

Case Study 6: Airports

Airports are typically regulated to some degree, and as such inflation sensitivity somewhat depends on the regulatory model of the airport. Most airports are dual-till, where aeronautical activities are regulated and non-aeronautical activities (sometimes referred to as commercial activities — e.g., retail concessions, food and beverage outlets and parking) are not. Here we show how both work for Aeroports de Paris (Exhibits 3 and 4).

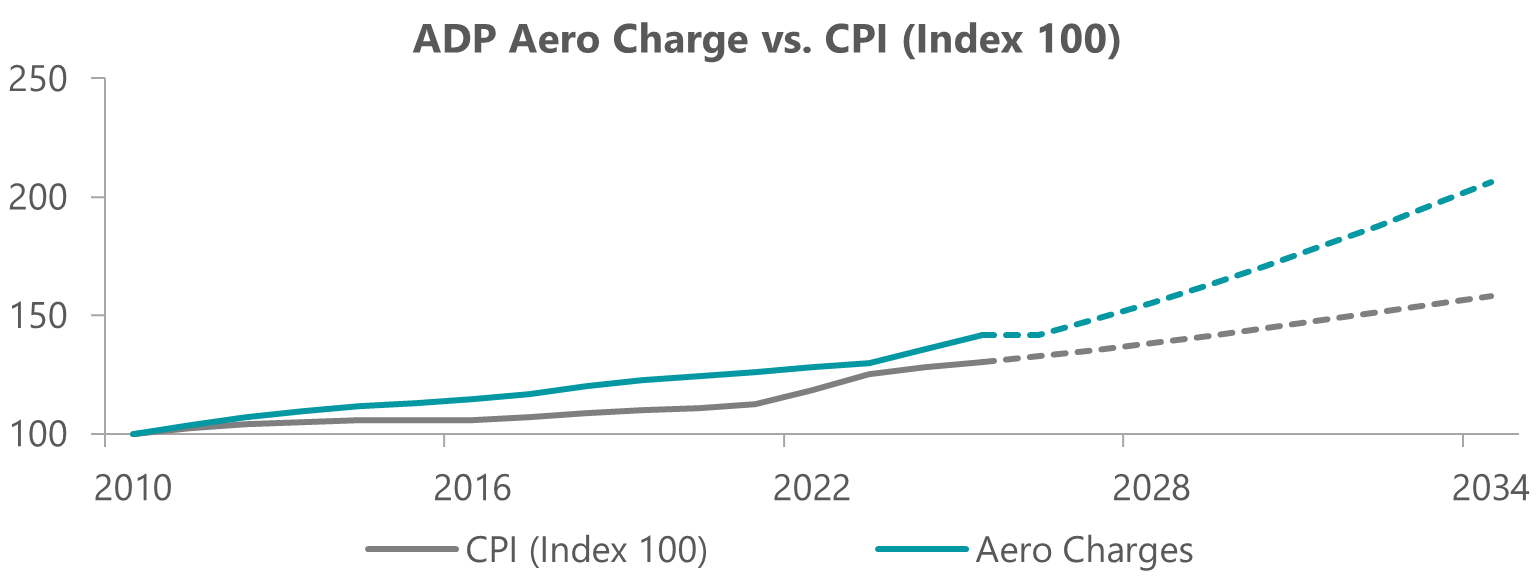

Exhibit 3: Aeroports de Paris Aeronautical Charges vs. Inflation

As of March 17, 2026. Source: ClearBridge Investments, ADP Financial Results.

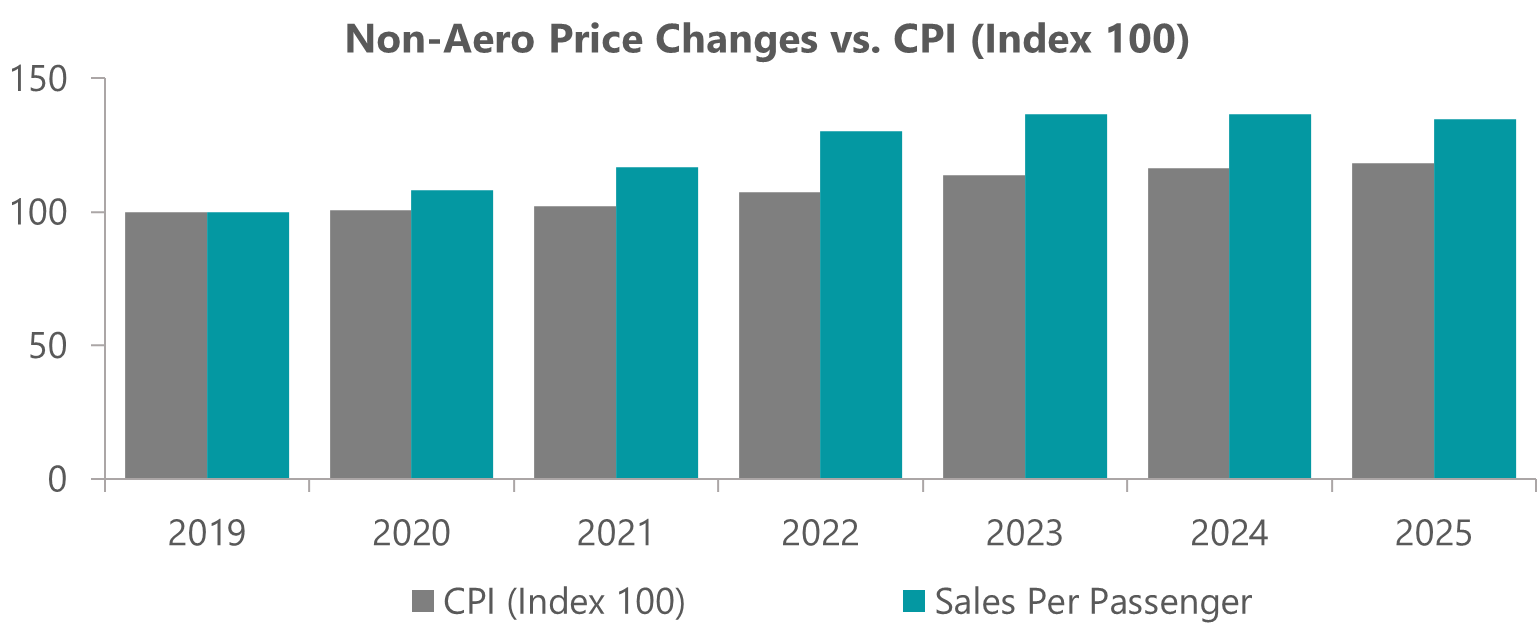

Exhibit 4: Aeroports de Paris Non-Aeronautical Charges vs. Inflation

As of March 17, 2026. Source: ClearBridge Investments, ADP Financial Results.

In general, both revenue streams can pass through inflation increases, although how this occurs varies:

- Aeronautical: Typically, regulators set an allowed return that regulated airport activities can earn. This allowed return is usually set for a period of five years and includes an estimate of inflation. Increases or decreases in the outlook for inflation are incorporated at the next five-year reset and flow through into regulated prices. Additionally, when setting prices for five years, price increases are often set as CPI + x, meaning prices are adjusted each year with inflation. As such, aeronautical activities can be exposed to inflation risk for up to five years, but in many cases have inflation linkages in actual pricing decisions.

- Non-aeronautical: Commercial revenues are usually negotiated between airports and customers. As such, short-term exposure to inflation is often dictated by contractual terms, while longer-term exposure is dictated by bargaining power. Historically, airport revenues have been able to achieve inflation via passenger increases on passenger-related activities such as retail and parking. Property revenue increases have often been above inflation given the scarce nature of airport land.

Many other factors also influence an airport’s ability to pass on price increases, including:

- Passenger mix: Increases in high-spending passenger groups such as Chinese tourists influence revenue outcomes.

- Foreign exchange (FX) rates: This is typically passed through immediately in short-term spending rates as most travellers have a budget in their home currency and their spending adjusts immediately with changes in FX. FX rates are often influenced by the relevant country bond rate expectations, which are also influenced by inflation.

- Passenger volume: Another key consideration in an airport’s ability to pass on inflation effects is passenger volumes, given that most revenue streams reflect the number of passengers multiplied by price. As such, ticket price changes can have effects on travel affordability and thus passenger numbers. Over the last 50 years, airline ticket prices have fallen in real terms often in combination with increases in disposable income, stimulating travel demand. To the extent airline ticket price trends change, this will also have an impact on headline revenue.

Conclusion

In a higher-inflation environment, particularly one driven by energy shocks, interest rates may remain elevated. However, many infrastructure businesses have embedded mechanisms that help preserve real cash flows over time, through explicit indexation, contractual escalators or regulatory resets. Overall, while the degree and timing of inflation pass-through vary by asset type, careful asset selection and an understanding of these pass-through pathways can help navigate inflation and higher rates.

Related Perspectives

Why Infrastructure Holds up Amid Middle East Inflation Pressures

Utilities in North America and Europe, pipelines and toll roads are positioned to withstand and grow through commodity-driven shocks such as the current Middle East conflict is creating.

Read full article