Although markets often pause to digest after large gains, history suggests these episodes usually prove fleeting, meaning major indexes could move higher in the second half of 2026.

Anatomy of a Recession

AOR Update: It's Looking Different

Key Takeaways

- With economic data continuing to surprise to the upside and a series of rolling sector recessions appearing to have failed to coalesce into a broader downturn, the ClearBridge Recession Risk Dashboard overall signal has improved to yellow from red. In tandem with this, our base case view is now that a soft landing is more likely than a recession in 2024.

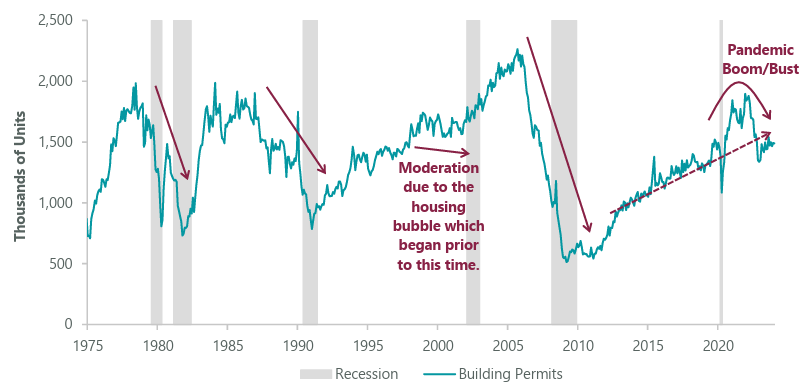

- Housing Permits have normalised from a pandemic-driven boom-and-bust cycle and in recent months have developed in a manner consistent with their pre-pandemic trend, resulting in this indicator improving to yellow from red.

- Given lofty valuations and earnings expectations along with a high chance of deceleration in economic momentum from above-trend levels, it would not be surprising to see a period of digestion for equities. Should recession risks continue to diminish, we believe long-term investors would be best served to take advantage of any weakness that emerges.

Pandemic Aftereffects Still in Play

The four most dangerous words in the investment industry are likely, “This time is different.” However, a review of the economic and market landscape since 2020 shows more differences than similarities to previous decades. The most striking difference has been the COVID-19 pandemic, a (hopefully) once-in-a-lifetime event. The impacts of stay-at-home and then reopening policies were not limited just to 2020, however, and had material aftereffects on the economy and financial markets. These dynamics continue to be a material driver at the industry level today, proving a challenge for traditional forms of analysis. While we are hesitant to say, “This time is different,” the events of the last few years — and perhaps more importantly the outlook for the coming year — are certainly looking different from history.

One of the most important aftershocks of the pandemic was the uneven timeframe with which different industries saw disruptions and then benefits from the pandemic. As a result, some industries’ business cycles became unsynchronised, creating what are called rolling sector recessions.

One example of this was technology, an early beneficiary during the 2020 stay-at-home period. Tech then became a relative loser to in-person services such as travel and dining out during the 2021 reopening and 2022 revenge-spending periods, when herd immunity allowed social distancing policies to be dropped. Several goods-focused industries, such as manufacturing and housing, also saw booms in 2020 that turned into busts in 2021 and 2022, while many services-oriented losers from 2020 became winners in 2021 and 2022.

Taking a step back, and with the benefit of hindsight, many areas of the economy look to be on trend with pre-pandemic patterns if the pandemic boom-and-bust cycle is removed. This is particularly evident in areas like total employment and housing, where housing permits for new construction are largely on pace with the pre-pandemic trend (Exhibit 1).

Exhibit 1: Building Permits for New Private Housing Units

Data as of 31 January 2024 most recent available as of 29 February 2024. Source: U.S. Census Bureau, retrieved from FRED, NBER.

The unsynchronised nature of rolling sector recessions meant that conditions ultimately failed to coalesce into a broader economic downturn in 2022 and 2023 despite consensus (and our) expectation of a recession. This presented a challenge for traditional economic analysis, as many industry-specific indicators saw sharp decelerations in growth that triggered recession warnings. With the benefit of hindsight, these indicators likely underappreciated the unsynchronised nature of the boom-and-bust cycles that were playing out in the economy due to the once-in-a-generation global pandemic.

For example, private fixed residential investment — aka housing — saw a string of nine consecutive quarters of negative contribution to GDP growth. In a more normal period, this reasonably would have been expected to coincide with a recession, as housing is an economically important sector with a large multiplier effect. This is because when individuals purchase a home there are many additional economic touchpoints, including construction workers, materials, real estate brokers, movers, furniture and appliances, and many others, leading to a large economic impact. When housing slows, typically the broader economy does as well, although we know the experience of the last few years was hardly typical.

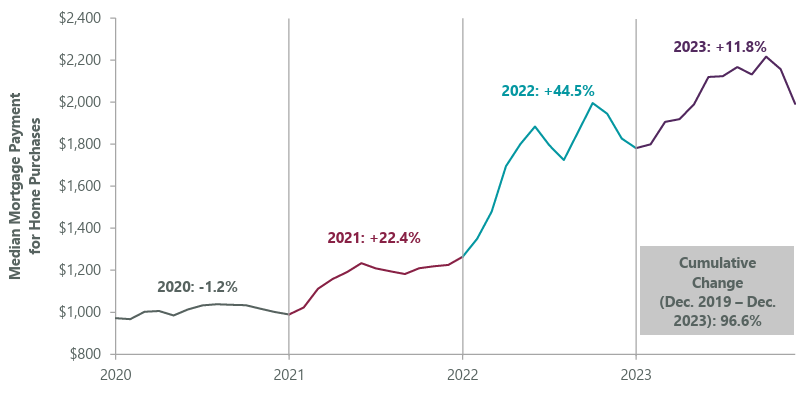

Further exacerbating the post-pandemic housing normalisation was the Federal Reserve’s most aggressive interest rate hiking cycle in roughly four decades. Housing is one of the most interest-rate-sensitive areas of the U.S. economy, given that most Americans finance the purchase of a home with a mortgage. After falling 1.2% in 2020, the payment for a mortgage on the median home in the U.S. rose by 22.4% in 2021, another 44.5% in 2022, and a further 11.8% in 2023, for an astonishing total increase of 96.6% since the onset of the pandemic (Exhibit 2). Put differently, the interest payment needed to buy the median home has effectively doubled in three years, dramatically outpacing the 26.1% increase in incomes over the same period, as measured by the Bureau of Labor Statistics’ Indexes of Aggregate Weekly Payrolls. As buying a house became less affordable, this market, which was already normalising following the pandemic boom, came under further pressure.

Exhibit 2: Housing: Bend or Break?

Median Mortgage Payment assumes August median existing home sale price (latest available) and September Freddie Mac mortgage rate. Data as of 30 December 2023. Source: FactSet, U.S. National Association of Realtors, and Freddie Mac.

Looking ahead, in terms of construction activity (which is key for economic growth), the housing market appears poised to build upon the recovery that began last year. According to ClearBridge’s Senior Analyst for Consumer Staples & Durables Robert Buesing, whose research includes homebuilders, supply chain improvement has helped bring the cost and timeframe associated with building a new home down relative to 2022. When combined with an outlook for a more stable (if not improving) mortgage rate backdrop and continued robust employment levels, this should be conducive to an overall pickup in residential construction activity in 2024.

With Housing Permits showing a continuation of the pre-pandemic trend, this indicator has improved to yellow from red this month, a notion supported by our colleague’s broadly positive outlook for future construction activity and its associated economic impacts. Even more importantly, this marks the fifth positive signal change in the last five months for the ClearBridge Recession Risk Dashboard and brings the total count to seven yellow and five red indicators. Simultaneously, the overall reading has now moved into yellow territory after nearing the threshold last month (Exhibit 3).

Exhibit 3: ClearBridge Recession Risk Dashboard

Source: ClearBridge Investments.

With this overall improvement in the ClearBridge Recession Risk Dashboard, our view is that a soft landing is now more likely than a recession in 2024, and our base case has flipped to soft landing as a result. To be clear, we believe that the economy is still going through the crux and the chances of a recession occurring are still meaningful. However, as we approach the two-thirds mark of the crux, economic data are clearly falling in the soft landing camp, with the Atlanta Fed’s GDPNow tracker reading 3.0% for first-quarter 2024 economic growth at month-end.

This is a tremendous outcome for the economy, although markets appear to have largely sniffed this out and priced in the soft landing already. To this end, the S&P 500 Index is currently trading at 20.5x expected next-12-month earnings, which are expected to grow at a more-than-solid 11.2%. With lofty expectations priced into equities, we would not be surprised to see a period of digestion emerge for equities, particularly given the prospect of slowing growth from elevated levels that could reignite recessionary fears even if a soft landing materialises. Ultimately, we believe long-term investors would be best served to take advantage of any weakness that emerges should recession risks continue to diminish.

Jeffrey Schulze, CFA

Josh Jamner, CFA

Related Perspectives

Anatomy of a Recession