An Active Bet on Emissions Reductions in Energy Sector

Key Takeaways:

-

The complexity of the energy transition is being underestimated, as evidenced by increasing power shortages and the potential for a full-blown energy crisis this winter.

-

ESG could be the best thing that ever happened to shale companies as it restricts investor capital, supports company discipline and forces companies to prepare for terminal demand.

-

The ideal market solution is higher energy prices while we transition from disciplined supply, as it will incentivize innovation and smart transition. However, underinvestment could result in energy spikes that derail or delay transition.

The focus of the energy transition is on shifting the incredibly complex power supply curve from thermal-based sources of energy to renewable energy, while still allowing demand for energy to keep growing. The complexity of this transition is being underestimated, as evidenced by increasing power shortages and the potential for a full-blown energy crisis this winter.

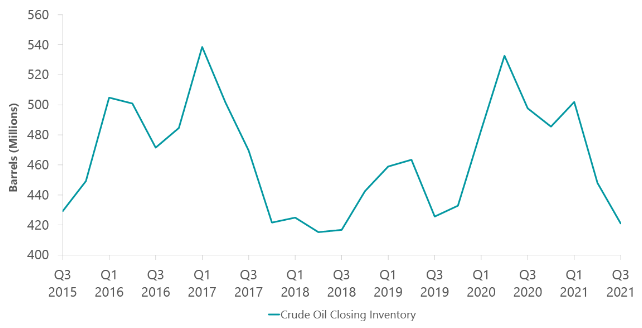

The challenge is that thermal energy supply is being cut back much faster than renewable energy can be delivered, coupled with short-cycle capital discipline and long-cycle underinvestment from oil and gas companies. With demand recovering cyclically, especially following the Delta wave, inventories are approaching recent lows (Exhibit 1) and spare capacity is declining. The result is a classic supply cycle for energy, without the usual supply response.

Exhibit 1: Crude Oil Inventories Drip Downward

Data as of July 31, 2021. Source: U.S. Energy Information Administration.

As active ESG value investors, we play a role in supporting the adaption to these massive changes. On the policy front we fully support a global carbon tax, which would provide a vital price signal to markets to reduce carbon supply and curtail demand and Scope 3 emissions — the real goal. A carbon tax would also generate revenues that will be sorely needed to fund the transition. We recommend portfolios undergo stress tests assuming different global carbon tax prices to get an understanding of the impact. What, for instance, would a $150 global carbon tax mean?

We are actively dialoguing and supporting our portfolio companies to reduce Scope 1 and 2 emissions, while still supplying markets with much-needed, but clean-as-possible thermal energy. For example, methane emissions (CH4) can be directly monitored and minimized and can have an outsize and much faster impact: CH4 can trap over 100x more atmospheric heat than CO2, and it dissipates roughly 10x faster. Cutting methane emissions in half by 2030 could avoid an estimated quarter degree of warming by 2050 and a half degree by 2100.

One of our main stock picking principles is focusing on companies that can successfully adapt to change. Besides minimizing Scope 1 and 2 emissions, the key adaption for energy companies has been the shift to free cash flow generation, allowing the companies to pay down debt and return capital to shareholders. As this is the first time shale energy companies have ever made money, the irony is that the incredible shale technological breakthrough was a near-death experience for these companies, which burned through over $200 billion in investor capital. Conversely, ESG could be the best thing that ever happened to the shale companies as it restricts investor capital, supports company discipline and forces companies to prepare for terminal demand. The result is that our energy company investments should generate the highest free cash flow and cash dividend yields in the market in 2022. Pioneer Natural Resources, for example, will pay a cash dividend of over 10% while achieving a fortress-like balance sheet that will allow stock buybacks. The ideal market solution is higher energy prices while we transition from disciplined supply, as it will incentivize innovation and a smart transition. However, underinvestment could result in energy spikes that derail or delay transition.

Today we see opportunity in the energy sector where we believe it is possible to witness adaptive change and get rewarded for it. The energy transition is effectively driving free cash flow yields that support much higher business values if they persist beyond the very short term, which we think is much more likely than what market prices currently embed.

Related Perspectives

ClearBridge Investments 2026 Stewardship Report

ClearBridge’s ninth annual report on our stewardship efforts explores our global platform for integrating sustainability factors across sectors, global and local markets, and the market cap spectrum.

Read full article